Eight housing associations have been reported to the regulator by official bodies more than once over the past five years because of repairs and maintenance concerns.

Statutory referrals are always considered by the regulator and they are made by authorities which include the Housing Ombudsman, tenant representative groups, MPs, councillors, the Health and Safety Executive, and fire and rescue authorities.

The regulator will look into a referral they will not necessarily take regulatory action.

Housing associations which were referred to the regulator more than once 2012-2017

Circle Anglia – nine referrals between January 2015 and December 2016 – referred by MPs, councillors, council (now part of Clarion)

Old Ford Housing Association – nine referrals between January 2015 and December 2016 – referred by councillors (now part of Clarion)

Circle 33 – three referrals between December 2014 and March 2016 – referred by MP, council, councillor (now part of Clarion)

Gallions Housing Association – two referrals in November 2013 and April 2015 – referred by tenants’ panel, MP (now part of Peabody)

Hyde Housing Association – two referrals in May 2015 – referred by tenants’ panel and ‘other’

Metropolitan Housing Trust – two referrals in November 2014 and June 2015

Places for People Group – two referrals in October 2014 and November 2014 – referred by councillors

Wandle Housing Association – two referrals in May 2012 and January 2015 – referred by MP and councillor

Source: Homes and Communities Agency response to an Inside Housing FOIA request

The Homes and Communities Agency has published guidance on a package of deregulatory changes for social landlords due to come into force in April. Measures include the removal of the constitutional consents regime, removal of the disposals consent regime and introduction of new notification requirements.

Until 6 April the Homes and Communities Agency will continue with the consents regime for both disposal and constitutional consents in line with the current statutory requirements.

The aim of the deregulation package is to remove English housing associations from the national balance sheet

The government has announced that £402m of funding over the next two years will be targeted at the councils with the greatest homelessness demand.

According to Inside Hosuing and government annoucemnts, CLG funding will replace the temporary accommodation management fee, which the government announced would be replaced in the Autumn Statement 2015. The funding will only be ringfenced for two years.

The government has allocated the funding by adding together the number of homelessness acceptances and prevention and relief cases achieved by securing a private rented sector tenancy.

There will be £186m in 2017/18 and £191m in 2018/19, with £25m set aside for London councils to work together to provide homelessness accommodation.

Under the existing system, funding can only be used when a household is already homeless, rather than being used to prevent this happening in the first place. Now, Councils could provide homelessness prevention support beyond 56 days

The new grant will allow councils to fund a wider range of homelessness services, for example employing a homelessness prevention officer to work with people who are at risk of losing their homes.

The new flexible homelessness support grant will replace the old system from April.

No council will receive less funding than they received under the old system, he added, and no council will receive less than £40,000 a year.

The government will set aside £25m of the funding for London councils across the next two years “in recognition of the particular challenges faced by London boroughs”. Before making final decisions on how this funding will be allocated the government will work with the Greater London Authority and councils “to consider ways of helping councils to collaborate in the procurement of accommodation for homeless households”.

Under the old system £40 per week for each temporary accommodation unit was available for London councils, and £60 per week for the rest of England.

The government will give £14m total extra funding to councils with high levels of temporary accommodation, including more than £1m for Westminster Council and £1.3m for Enfield Council.

Brighton and Hove Council will receive the largest allocation in the country outside London, with £6.1m.

The government has frozen the work of the RTB initial pilots in favour of waiting for a regional pilot. No news yet on where that will be

This was the exerpience of the smaller pilot:

According to inside Housing:

“A quarter of eligible tenants expressed an interest in buying their homes under the Right to Buy extension pilot, but affordability acted as a major drag on actual sales.

The final analysis of the Right to Buy pilot scheme, run by five landlords last year, was published by academics at Sheffield Hallam University.

It showed 4,405 expressions of interest were made, but this led to 972 formal applications and 81 sales, meaning a total of 5.9% of eligible tenants applied to buy.

The report confirms the level of demand.

The pilot scheme was run across areas where the participating housing associations owned 53,955 homes with tenants with 10 years’ residency eligible to buy.

However, more than 17,000 of these properties were excluded at the outset with homes built under Section 106 planning rules, rural properties and supported housing automatically excluded.

Hugh Owen, director of policy at Riverside, said managing expectations – particularly among tenants living in excluded homes – was a key challenge for the associations engaged in running the pilot.

In the main scheme associations will be free to include or exclude properties, and will be obliged to offer an alternative property for those excluded. Eligibility may also change.

However, in the pilot scheme these restrictions left 16,386 properties with eligible tenants in non-excluded properties.

In the London pilot, operated by L&Q, more than 1,800 expressions of interest were made in the first two months of the scheme – well ahead of other areas. This led to a decision to “pause” the scheme causing “considerable frustration among those being held back in the queue”, according to the research.

The academics also cited delays in passing the Housing and Planning Act, processing applications and instructing solicitors in contributing to the lower-than-expected level of completions.

However affordability, particularly in London and the South East, was cited as a major drag on sales with the average household income among applicants £32,000 per year.

Despite these restrictions, tenants were able to secure mortgages at high rates and some worked overtime and second jobs in a bid to buy, prompting warnings about unsustainable levels of financial risk.”

Figures on housing association development are not independently recorded by government. The NHF is collecting development figures from members to provide an authoritative update on the sector’s output.

According to Inside Hosuing:

“The regional figures show 11,000 homes completed in London with 11,500 starts. By comparison, in the North East, associations completed only 900 homes, with 1,000 homes started.

Since grant levels were slashed in 2010, housing associations have been reliant on generating profits through boosted rents and sales to fund development. In lower-value areas this is more of a challenge.

In its regional reports, Home Truths, the NHF said: “Our homes are for everybody – from those most in need, to young people, families and first-time buyers, to older and more vulnerable people who may need support. We’ll continue to deliver across the mix to meet changing housing needs.”

Government net additions figures show only 32,110 affordable homes were added to the housing stock in 2015/16 – the lowest level since 1992. The figures do not break down the homes built by tenure.

An outstanding approach to promoting digital inclusion

Blackwood Homes and Care

Derwentside Homes

East Thames

Halton Housing Trust

Pickering & Ferens Homes

Sentinel

Soha Housing

An outstanding approach to regeneration

Hull City Council and Keepmoat

Liverpool City Council

Manchester City Council, Keepmoat and Guinness

Metropolitan

Network Homes

Newlon Housing Trust

Poplar HARCA

Together Housing Group

An outstanding approach to repairs and maintenance

A2 Dominion and Mitie

Genesis Housing Association

Hyde Group

North Lanarkshire Council

Riverside

Shoreline Housing Partnership

Wales & West Housing

Wandle

An outstanding approach to tackling anti-social behaviour

Clarion Housing Group

Corby Borough Council

Newham Council

North Tyneside Council

Stockport Homes

An outstanding approach to tackling homelessness

Crisis

Croydon Council

Depaul

Evolve

Hyde Group

Lewisham Council

New Charter Group

OVO Foundation and 1625 Independent People

Stockport Homes

Wigan & Leigh Homes

An outstanding approach to tenant involvement

Belle Isle Tenant Management Organisation

Derby Homes

Guinness Partnership

Hull City Council

Maryhill Housing Association

Ongo

Phoenix Community Housing

Soha Housing

Outstanding campaign of the year

Amicus Horizon

Ashley Community Housing

Carmarthenshire County Council

Housing Executive

Merlin Housing Society

MHS Homes

North Lanarkshire Council

Outstanding development programme of the year

Aster Group

Blackpool Housing Company

Coastline Housing

ExtraCare Charitable Trust

Home Group

Hull City Council

L&Q

North Kesteven District Council

Swan Housing Association

Yarlington Housing Group

Outstanding innovation of the year (over 20,000 stock)

Bromford

Family Mosaic

Housing Executive

Orbit Group

Places for People and FCS Energy

Hyde Group

Thirteen Group

Wigan & Leigh Homes

Outstanding innovation of the year (under 20,000 stock)

Blackpool Housing Company

BPHA

Choice Housing Ireland

Housing and Care 21 and Appello

Lewisham Council

Loreburn Housing Association

North Tyneside Council

Poplar HARCA

RHP Group

Outstanding landlord of the year

Amicus Horizon

Greenfields Community Housing

Ongo

Queens Cross Housing Association

Soha Housing

South Cambridgeshire District Council

Stockport Homes

Wales & West Housing

Outstanding strategic local authority of the year

Bournemouth Borough Council

Hackney Council

London Borough of Waltham Forest

Newcastle City Council

Nottingham City Council

Teignbridge District Council

West Lothian Council

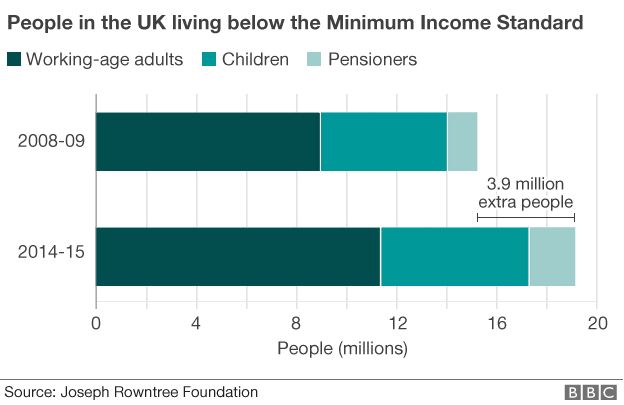

According to the BBC – nearly a third of the population of Britain is living on an “inadequate” income, according to research by the Joseph Rowntree Foundation (JRF).

In 2014-15, it said that 19 million people were living on less than the Minimum Income Standard (MIS).

It said the problem was that household costs have been rising, while incomes have stagnated.

The government has already promised to tackle the issue, after Theresa May identified those “just about managing”.

It said it was taking “targeted action” to raise incomes.

The MIS is set by experts at Loughborough University, and is based on what members of the public think is a reasonable income to live on.

Although the precise level depends on individual circumstances, a single person renting a flat outside London is said to need to earn at least £17,300 a year to reach the MIS.

For a working couple with two children, living in social housing, each of the individuals needs to earn £18,900 a year.

In other words a couple could be earning £37,000 jointly, and still count as being below the MIS threshold.

Poverty

Among the 19 million said to be below the MIS are six million children, representing 45% of all children in Britain.

There are also 1.8 million pensioners, representing 14.6% of the age group.

The figures are up from 15 million, or 25% of the population, six years previously.

The report warns that many of the families that are just about managing are in danger of falling into poverty.

That is despite record levels of employment.

‘Money is always in the background’

Lynn Williams and her husband Derek live in Glasgow. They class themselves as “just about managing”.

They receive some disability benefits, a small income from a works pension, and Lynn works part-time.

But they only survive by dipping in to savings.

“We do worry about money constantly; it’s always in the background,” says Lynn.

“There’s only so often your savings can be dipped in to. But we are lucky. Other people can’t even afford to put their tumble driers on.”

The JRF said that the price of a minimum basket of goods had risen by up to 30% since 2008, while average earnings had risen by half that amount.

However, more recent figures suggest that wages have been rising faster than inflation for more than two years.

Average weekly earnings have risen faster than CPI inflation every month since October 2014, according to the Office for National Statistics.

But many expect wages to fall below inflation again in the months ahead.

“This could be a very difficult time for just-managing families as rising inflation begins to bite into finely-balanced budgets,” said Campbell Robb, the new chief executive of the JRF.

“The high cost of living has already helped push four million more people below an adequate income, and if the cost of essentials such as food, energy and housing rise further, we need to take action to ease the strain,” he said.

Minimum Income Calculator

Image copyrightRAWPIXEL

Click here to see what the Minimum Income Standard is for your type of household.

Wage growth

However the government said it was taking “targeted action” to raise incomes.

It said that last year the lowest paid saw wages rise by 5.6% in real terms, the biggest increase since records began in 1997.

And it pointed out that the National Living Wage would go up to £7.50 an hour from April.

“We’re determined to build an economy that works for everyone and we are taking decisive action to help with the cost of living,” said a government spokesperson.

“A million workers have had a pay rise thanks to our National Living Wage, and we have delivered the fastest wage growth for the lowest paid in 20 years, taken millions of people out of tax altogether and frozen fuel duty for seven years in a row.”

The NHF are suporting As by writing to them about some developments which may lead participating employers of the Social Housing Pension Scheme (SHPS) to change the way in which they account for the defined benefit (DB) section of SHPS.

The SORP Working Party (SORP WP) is developing a methodology to understand if necessary information could be determined that could enable all housing associations that are members of SHPS to account for their portion of the SHPS deficit as a DB scheme. The SORP WP is undertaking this on behalf of the sector to reduce the financial and administrative burden on housing associations as it is likely that recent developments in the sector may require every housing association to individually approach a professional actuary to calculate their portion of the SHPS deficit.

Background

Prior to the transition to FRS102, housing associations were able to take advantage of a multi-employer exemption in FRS 17 and as a consequence SHPS deficits were not reflected in the sector’s accounts. Instead, housing associations accounted for SHPS as if it was a defined contribution scheme (DC) – essentially for the pensions contributions paid in the year only.

Since the transition to FRS 102, a similar exemption allows housing associations to account for SHPS as a DC scheme and in doing so bring onto the balance sheet the present value of the deficit recovery plan. This treatment recognises that information is not available from TPT to allocate scheme assets between participating employers and therefore it is not possible to obtain sufficient information to account for SHPS as a DB scheme.

For completeness, the DC section of SHPS is not included in this review. In addition, accounting treatments under other accounting standards such as IAS19 are also out of the scope of this review.

Recent Developments

In spite of the FRS102 exemption, it is the SORP WP’s understanding that a number of housing associations are considering approaching professional actuaries to estimate their share of the SHPS assets, liabilities and hence SHPS deficit. These housing associations are confident that as a result of this process they will have sufficient information to account for SHPS as a DB scheme for the financial year ending 31 March 2018 and beyond.

Auditors on the SORP WP noted that if some housing associations were able to adopt an approach to account for SHPS as a DB scheme, this may indicate that sufficient information was more widely available to enable other employers to also do so. This would depend on individual employer circumstances and materiality.

Meeting with TPT and TPT’s Actuaries

Members of the SORP WP recently asked TPT and TPT’s actuaries, Jardine Lloyd Thompson (JLT), for details of the information that is available. As a result, the SORP WP has started work on developing a methodology that may enable sufficient additional information to be calculated or estimated to achieve DB accounting. In addition, the SORP WP will consider how assurance could be provided on the methodology and information produced for housing associations centrally, for housing association auditors to then rely on. This will reduce the added cost of every housing association auditor requiring assurance on each set of housing associations’ SHPS figures.

Costs

The SORP WP believes there will be four costs associated with this work

1. The development of the initial methodology – this is likely to take several weeks and will involve a professional actuary and liaison with TPT, JLT and several audit firms

2. The implementation of the framework for the provision of the information (for example the development of a TPT online system)

3. The extra costs for TPT to run the methodology on a periodic basis

4. The cost of providing central assurance on the annually generated information.

Whilst the above would be a matter for the SHPS Committee to engage employers on, we anticipate that these costs will be shared amongst those organisations that are members of SHPS. The SORP WP expects the costs will likely vary to some degree by the size of each housing association’s deficit however the exact cost framework still needs to be developed. The first year cost will be higher than the following years because of the added expense of developing the methodology, implementing the framework for the solution and calculating the position for prior years. The overall cost of this approach for the sector will be significantly lower than the outlay if each housing association separately engaged a professional actuary to generate the information and the added cost of having this information audited.

A new session at the Federation’s Finance Conference<http://national-housing-federation.org.uk/3R33-5YU3-1NXVF8-2ZJS5-1/c.aspx> has been developed to provide further details on the progress with the methodology (a SORP WP meeting is being held the day before the conference to discuss the methodology):

Pensions Accounting – DB or not DB

Hear from members of the SORP Working Party on developments that might enable SHPS DB schemes to be fully accounted for as DB schemes on Balance Sheet. This session will go through the current treatment of the SHPS DB scheme under FRS 102 and progress being made on the development of a methodology to enable full DB accounting and what this could mean for your organisation’s pensions disclosures.

You may have heard of some HAs working in 2016 on a Sector Scorecard, a new way of benchmarking efficiency across the sector. SomeHAs are now being asked to join a wider pilot.

What is the Sector Scorecard?

The working group, led by Home HA are proposing 15 measures split across five categories: business health, development (capacity and supply), outcomes delivered, effective asset management, and operating efficiencies. Some contextual information will also be collected to present an overview of the housing association and assist with selecting peer groups to measure against.

The indicators have been chosen to build a meaningful picture of associations, and this is information that most organisations will already be gathering.

The project has sector-wide backing with support from:

• National Housing Federation

• Chartered Institute of Housing

• G15

• PlaceShapers

• g320

• Homes for the North.

The Government also supports the project, with the Housing Minister saying:

“I welcome this initiative to develop a set of common efficiency metrics for the housing association sector. The sector has a vital role to play in providing the homes we need, and housing associations need to be able to demonstrate that they are making the best possible use of their resources to deliver for the communities they serve.”

Julian Ashby, Chair of the HCA Regulation Committee, has also said that the HCA will consider scrapping VfM statements if it can rely on common ’metrics‘ to measure efficiency.

This is a useful summary, we can expect powers for Councils to appoint and use their golden share on HAs to be interveed by the CLG; we can expect mergers, followed by an in depth assessment, rtaher than HCA permisison for structurla changes in HAs and we can expect HAs to no longer have regulatory requirements to seek permisison to sell their homes.

Seperately, the HCA is consulting on a revised tenant involvement standard to ensure when deregulation is gone that where decisions impact on tenants they are fully consulted